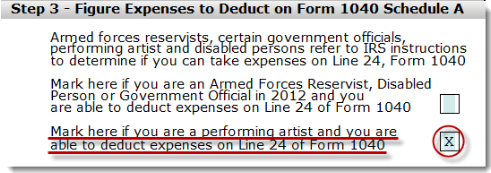

Employee Business Expenses For Qualified Performing Artist Not Carrying to Form 1040

There are certain requirements that first must be met in order to deduct employee business expenses for qualified performing artists on Form 1040.

1. The Adjusted Gross Income must be $16,000 or less before deducting expenses as a performing artist.

If the amount on Form 1040 line 37 is greater than $16,000, the artist is not considered a qualified performing artist and cannot deduct business expenses on Form 1040. The expenses can still be deducted on Schedule A under Other Miscellaneous Deductions.

2. The artist must perform services in the performing arts as an employee for at least two employers during the tax year.

3. The artist must receive from at least two of those employers wages of $200 or more per employer.

4. The artist must have allowable business expenses attributable to the performing arts of more than 10% of gross income from the performing arts.

5. In addition to the above requirements, Form 2106 must be marked as belonging to a qualified performing artist.